This week’s blog post points to my latest YouTube video where I share an update on my two taxable dividend income portfolios.

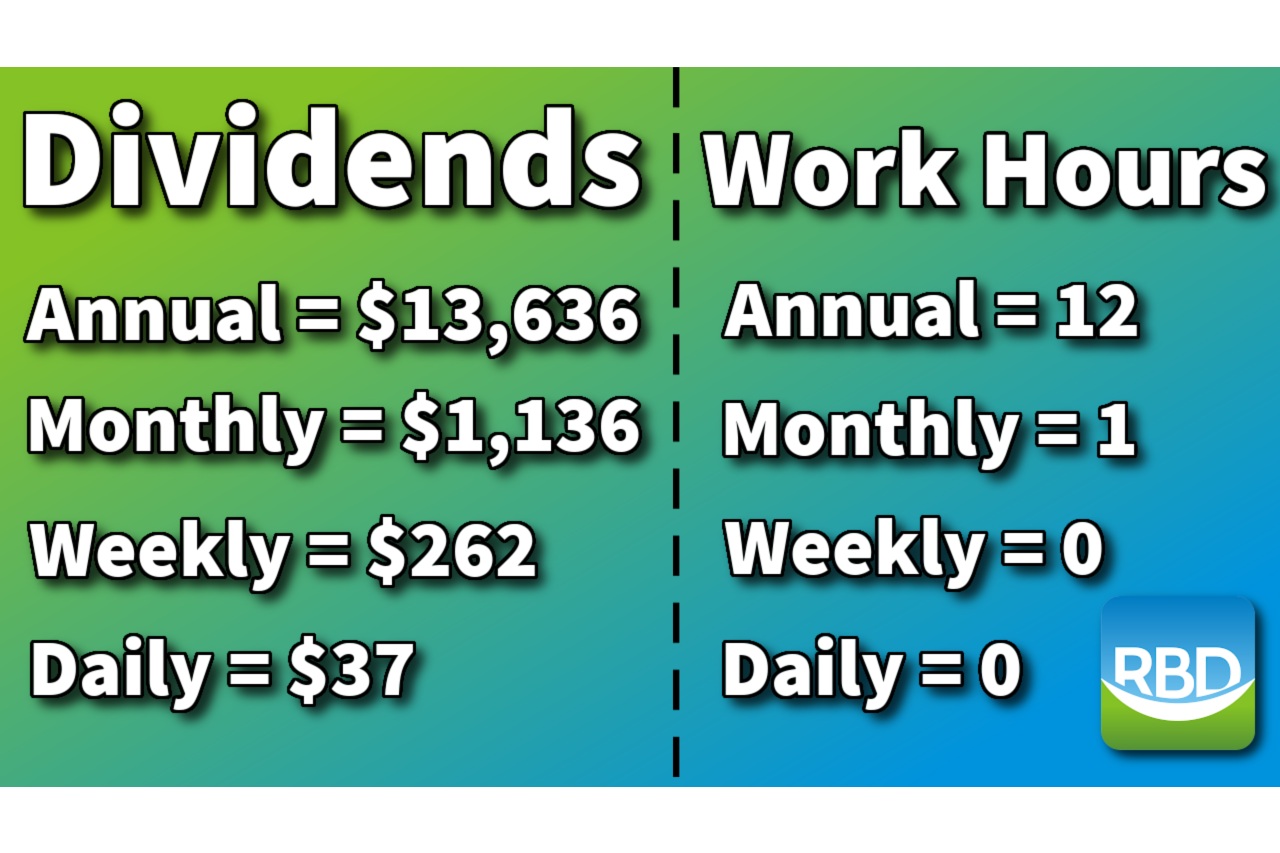

The combined portfolio pays me about $13,633 per year in dividend income or about $1,136 per month.

The video shows my Fidelity and M1 Finance portfolios and a combined future dividend income view using Stock Rover — a portfolio tracking and research platform.

I’ve shared that we use this portfolio for living expenses when our monthly spending exceeds our income, which is variable now that I’m self-employed.

Having an income portfolio like this was one reason I was confident enough to leave my full-time job.

This portfolio is a valuable asset, and I’m pleased about all the spending sacrifices I made to build it.

But if I were starting from scratch, I’d do things differently. Most of my content today reflects the preferred and less time-consuming approach of using index funds and ETFs instead of individual stocks to build retirement security.

Yet, I still own many individual stocks, and I’m simplifying my portfolio as I approach retirement.

Here’s the video if you want to view the portfolio. Read more about this portfolio after the video.

How it Started

Long-time RBD readers (some of you date back to 2013!) may remember regular updates on a dividend stock portfolio I was building for passive income.

Readers still ask me about this, though many are probably long gone since I stopped sharing this information around 2016.

I started investing in dividend stocks in 1995. Back then, dividend reinvestment plans (DRIPs) were the only way to invest small amounts of money (as low as $25) without the penalty of excessive trade commissions.

My Uncle was the stock transfer agent at Chevron, and he set me up with a DRIP account.

I invested by mailing checks for the first few years.

By 2013, I had a decent amount invested. The blog motivated me to accelerate additions to the portfolio over the next decade as my income grew.

I prioritized retirement contributions first, including employer-sponsored plans, IRAs, and Roth IRAs.

My savings rate was high enough to max out retirement accounts AND make substantial investments ($1,000-$5,000 each month) into the non-retirement taxable accounts.

I made decent money but have always kept our expenses low, especially with housing and cars.

Several other bloggers provided similar updates, and we all cheered each other’s progress. Some bloggers still do this.

Eventually, the explosive availability of low-cost, low-minimum mutual funds and ETFs ignited the FIRE movement, and many DIY investors shifted to a more passive index fund investing strategy.

Now, income-focused portfolio builders use low-cost dividend ETFs like SCHD and VYM to build diversified passive income without the burden of stock research. Videos on these ETFs are all over YouTube.

My initial early retirement plan (to retire at age 55) required heavy investing into income-producing assets to provide supporting income between age 55 and 59 1/2.

Now that I plan to continue working past 55, passive income during that period is less of a concern.

But I also saw a passive income portfolio as a valuable long-term retirement asset, requiring fewer withdrawals from my traditional and Roth retirement accounts, allowing them to grow as I lived off dividends or drew down the taxable portfolio.

The value and flexibility of this portfolio asset are playing out today after almost thirty years.

How it’s Going

All those years of maxing out retirement accounts paid off. My retirement accounts have substantially exceeded the value of my taxable accounts. I can tap those accounts in a decade.

The taxable accounts at Fidelity and M1 Finance have become less exciting.

With the smaller portfolio at M1 Finance, I reinvest the dividends into ETFs.

The Fidelity dividends are a different story, as I’m not reinvesting the dividends back into the portfolio.

When needed, I withdraw dividends to cover living expenses.

But I’m transferring surplus dividends from the Fidelity taxable brokerage to my Fidelity Roth IRA.

This maneuver will likely become the topic of a future blog post and video.

Since I’m spending most of my business income, I don’t have as much savings to contribute to our Roth IRAs directly.

But the surplus dividend is a perfect source as long as I have the cash available to transfer. In-kind stock transfers are not allowed.

The other limitations are the standard Roth contribution limits ($8,000 for 50+ in 2025, like me) and eligibility, which keeps increasing.

The upper limit on income eligibility is a modified adjusted gross income of $246,000 for married filing jointly. I’m not too worried about meeting that threshold while self-employed. If I do, I can always remove ineligible contributions before tax time.

So, I’m making $500 contributions each month, using a dollar-cost averaging instead of a lump sum (to maintain some flexibility and wait for dividends to populate my account).

I’ve set this up on autopilot, automatically transferring and investing contributions into a growth ETF.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

Morningstar Investor — Trusted fund and ETF research + portfolio tracking. 7-day free trial.

Sure Dividend — Research dividend stocks with free downloads (review):

Fundrise — Simple real estate and venture capital investing for as little as $10. (review)

Publisher: Source link