Key retirement costs are being overlooked by many Americans. (Maybe not you though, especially if you are a NewRetirement Planner subscriber, but, keep reading to make sure.)

According to a survey by the Employee Benefit Research Institute (EBRI), fewer than 50% of Americans “have planned for emergency expenses or calculated how much is needed to cover health expenses” in retirement.

And, the Society of Actuaries found that while more than six in ten pre-retirees and seven in ten retirees have given at least some thought to how their lives will change throughout retirement, only 16% of pre-retirees and 27% of retirees feel very prepared for financial events in the future. Pre-retirees are more likely to feel not too or not at all prepared than retirees (29% vs. 17%).

Here is a full rundown of the top 10 critical but overlooked costs in retirement planning – and what to do about them.

1. The Most Important Retirement Costs: The Fun Stuff

It may seem surprising, but people are apt to leave the good (fun) stuff out of their projected retirement budgets.

The EBRI report suggests that only about half of retirees say that their lifestyle is about what they planned it would be before they retired. And, many report that their overall spending and expenses, particularly travel expenses, are higher than expected after they retire.

Travel, personal care, hobbies, gifts for friends and family, and all the things that make retirement worthwhile are too often not budgeted appropriately before retirement.

What’s worse, these costs can quickly add up and could cause major financial issues later in life if they have not been accounted for.

How to Plan for the Retirement You Dream Of

The detailed budgeting feature in the NewRetirement Planner is a good way to imagine future retirement costs. There are over 75 categories and you can set spending for each category for different time periods.

Do you dream of travel? Set a specific budget for it. You can put in an annual or monthly expense. And, budget annually or every other year for your lifetime or just the first few years of your retirement.

If you don’t want to use the budgeter and have a few big purchases, use the one time expenses feature to factor in sizable purchases.

2. Inflation

The one benefit of the currently high inflation rate? We have all learned (or relearned) that inflation can be a big deal – especially after retirement when your fixed income and resources may not keep pace with the increased costs of goods and services.

Inflation makes things cost more, reducing the amount you can buy. If you want future financial security, you have to factor inflation into your spending projections.

How to Plan for Inflation

When projecting your future finances, inflation is a critical consideration. In fact, it is one of the most important inputs for your calculations. Your future spending and chance of affording retirement may be very different if you are projecting using a 2% vs. 8% inflation rate.

You should calculate your future financial security using assumptions for inflation that make you comfortable with your projections. However, you don’t necessarily have to use the recently high rates of 8-9%. Instead, consider using a number that reflects a long term projected average.

The NewRetirement Planner enables you to set both an optimistic and pessimistic rate of inflation. You can toggle between your projections with the different rates. Some people look to long term averages to help them set their rates and use:

- 2.5% for an optimistic long term rate

- 4-5% for a pessimistic long term rate

NOTE: The average yearly inflation rate in the US from 1960 through 2023 was 3.8% per year. And, some say that we are better at monetary policy now than we were before. The average inflation rate over the past 30 years was 2.27%.

In addition to enabling you to set a pessimistic and optimistic rate for general inflation (the costs of most goods and services), the NewRetirement Planner enables you to input rates for:

- Medical inflation (healthcare costs have increased at a faster rate than general inflation)

- Housing (housing appreciation is generally a good thing if you own the asset, but housing can also be a cost)

- Monetary Assets (your rate of return for investments)

- Other assets (for example, the appreciation or depreciation rates for homes and other non-monetary assets)

3. Future Maintenance Costs

Though you may have stopped punching a clock at work, time marches on in retirement. If you own a home or a car, you’ll have to maintain those assets, just like you did before. The roof will need work at least one more time, and you could roll another 50,000 miles on your car.

Unfortunately, calculating future maintenance costs is more difficult than figuring out the depreciation of your property and its replacement value.

Accidents are also a future hazard, and with the increase in extreme weather events around the world, you can bet trees will blow down, rains will erode your foundations and extremes of hot and cold will crack your pavements.

How to Plan for and Predict Maintenance Costs

It is recommended that you create a detailed budget for your future retirement spending. The NewRetirement Planner allows you to enter spending and how that spending will change in hundreds of different categories.

For example:

- You might enter a one time expense for roofing

- A yearly expense for yard and general maintenance

- Regular car maintenance or a future car purchase

The NewRetirement detailed budgeter can help you think through your maintenance costs in a variety of different categories.

4. Emergency and Other Unforeseen Costs

The only thing you can almost guarantee is that the unexpected will probably happen. But, how do you predict and plan for what you don’t know will happen?

It is not a trick question, and there are no easy answers, but you have ways to protect yourself.

How to Predict and Plan for Emergency Costs

While you can’t predict the future, you can plan for the possibility of an emergency. It is recommended that you:

- Retain an emergency fund

- Make sure you carry adequate insurance

- Build flexibility into your overall retirement plan

5. Taxes

According to the Tax Foundation using the recent information, the average federal income tax paid was:

- $10,649 by all taxpayers

- $643 by the bottom 50%

- $20,645 by the top 50%

- $36,907 by the top 25%

- $75,406 by the top 10%

- $126,604 by the top 5%

- $412,846 by the top 1%

Now, multiply the applicable number by 20 (or, the number of years you might be retired) and you’ll see that taxes are a big retirement expense and you need to plan for the costs. Luckily the NewRetirement Planner factors taxes and helps you plot to reduce the expense.

Tax Planning for Retirement

The NewRetirement Planner has – by far – the most sophisticated, detailed and reliable tax planning engine. It factors taxes into your projections automatically.

The model encompasses current federal and state income taxes and deductions, realized gain modeling and more. The Tax Insights chart enables you to see:

- Gross taxable income by source, which can vary between Federal and State tax calculations

- Deduction modeling each year, either itemized or standard — whichever will reduce your estimated taxes the most

- Marginal tax rate reporting so you can identify the years when you may have the highest and lowest tax rates

The modeling ensures that you are anticipating the costs. It also enables you to see opportunities to reduce the expense. Try QCDs, itemizing deductions, reducing income to stay under certain brackets and doing Roth conversions.

The Roth Conversion Explorer, part of PlannerPlus can help you identify a personalized strategy for doing conversions. (Want to know if you should convert this year? Use this stand alone Roth Conversion Calculator.)

6. Healthcare

Don’t assume that Medicare will cover all your medical costs in retirement.

According to the 2024 Fidelity Retiree Health Care Cost Estimate, a 65-year-old individual may need $165,000 in after-tax savings to cover health care expenses. The estimate is $315,000 for a couple.

How to Plan for Out-of-Pocket Medical Costs

Be sure to use the NewRetirement Planner to get a personalized estimate of your out-of-pocket medical costs using your zip code, the types of coverage you have and plan to have, your medical conditions, and more.

7. Long Term Care

The costs of long term care are exorbitant and are not usually covered by Medicare. The rates vary widely by location, but, according to Genworth, the national average annual costs are around:

- $20,300 for adult day care

- $54,000 for a private one bedroom in assisted living

- $59,500 for homemaker services

- $61,750 for a home health aide

- $95,000 for a semi-private room in a nursing home

- $108,500 for a private room in a nursing home

And, you may need to double the above expense estimates to estimate your lifetime costs. A report jointly prepared by the American Health Care Association and National Center for Assisted Living found that the average length of stay for residents in an assisted living facility is about 28 months with the median being 22 months or nearly two years.

How to Plan for the Possibility of Long Term Care Costs

Unfortunately, long term care insurance can be costly and inefficient. However, you have additional options. The NewRetirement Planner can step you through some possibilities and enable you to plan for the costs. Or, explore 10 ways to cover long term care costs beyond insurance.

8. Retiring Sooner than You Expect

If you are forced to retire earlier than expected, you are faced with extra years during which you’ll need to cover the costs with your retirement resources.

The Society of Actuaries found that today’s pre-retirees plan to retire at a considerably older age than current retirees. The actual median retirement age is 60, yet two in 10 pre-retirees said they plan to work at least until age 68 and 14% said they do not plan to retire at all.

While that’s an admirable goal, the fact is that many seniors are unable to continue working past normal retirement age.

And, surveys from the Employee Benefits Research Institute have shown that about half of retirees left the workforce before they were ready. And, many have jumped ship early due to the pandemic.

How to Plan for a Forced Retirement

If you are planning on working past 60, you might try to run a scenario when you are forced to quit work earlier. See if your finances will last and explore what adjustments you might need to make.

Many retirees who find themselves with an earlier than expected retirement turn to “bridge employment,” a job that may be part-time and pay less, but helps bridge the gap between their last job and full-time retirement.

There are some great ideas here: 9 tips for surviving a job loss near retirement age.

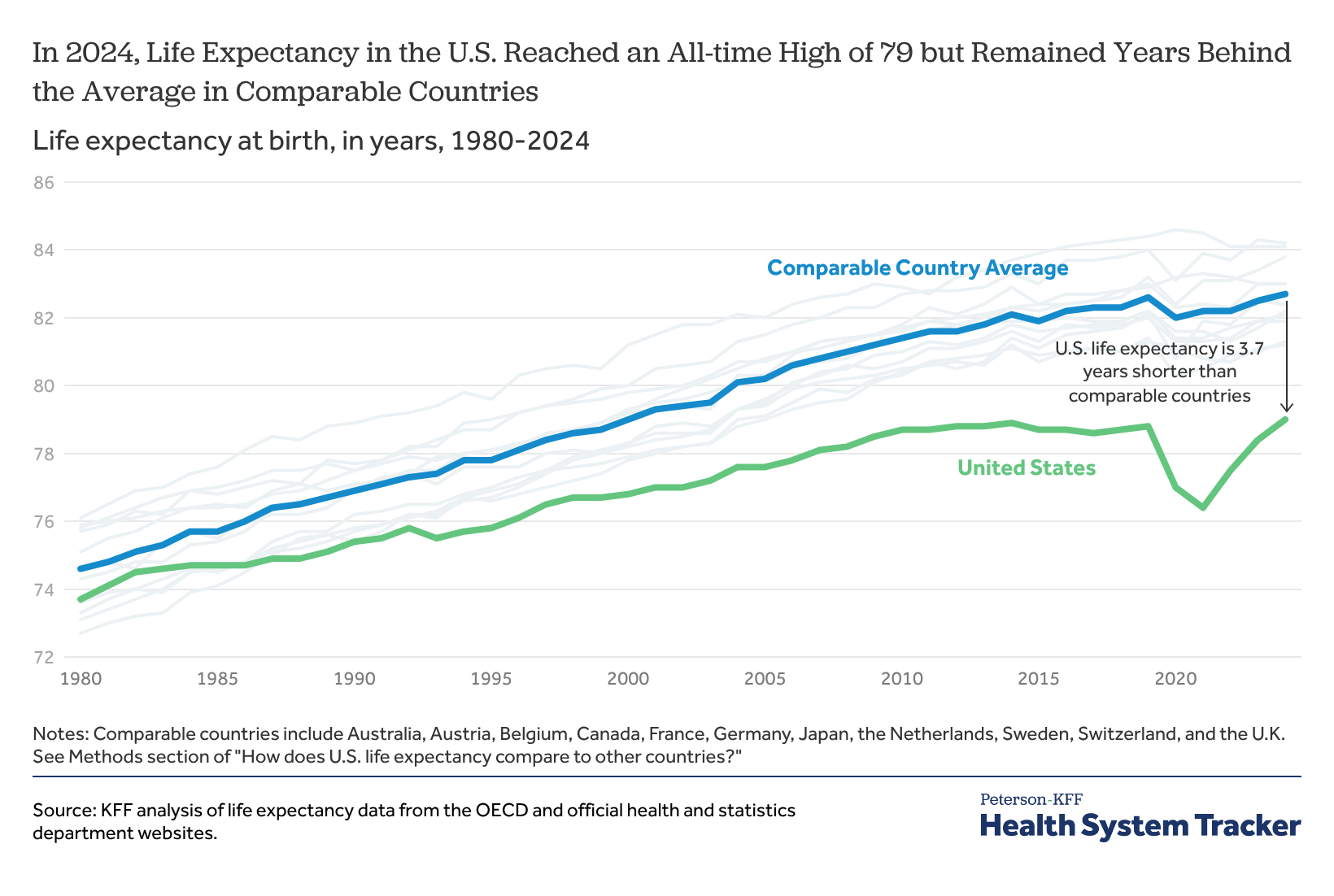

9. Longevity

How long you live is the biggest wildcard of all. You may think budgeting your money until your 100th birthday is fine – until your 101st birthday rolls around.

Life expectancy in the United States has soared from 70 years in 1971 to around 80 years in 2020, and advances in medicine could keep those in their 40s and 50s today alive well into their 80s and 90s. Every year is a gift and an extra cost that must be planned for.

While the average life expectancy for Americans has dropped in recent years, the losses are not even across demographics.

How to Plan for a Long Life

You can use a life expectancy calculator, actuarial tables, or just take a guess at how long you will live based on your parents’ longevity. However, it is probably a good idea to make your money last a bit longer than you think you’ll live.

10. Sandwich Generation Costs

The so-called “sandwich generation” – usually baby boomers – are people who are caring for their elderly parents while simultaneously financially supporting their adult children.

A study from AARP found that:

- 32% of midlife adults ages 40–64 provided regular financial support to their parents in the past year, 42% expect to be doing so in the future.

- Half of midlife adults are still providing money to their adult children age 25 or older (51%) for basic expenses.

Providing this care can be costly, both in cash outlays, but also in lost wages.

How to Plan for Costs Associated With Other Family Members

Creating a detailed budget is perhaps the most important aspect of retirement planning. You want to know what money you will need and when.

The Budgeter in the NewRetirement Planner helps you think through costs associated with family members — and many other potentially overlooked retirement costs.

Publisher: Source link