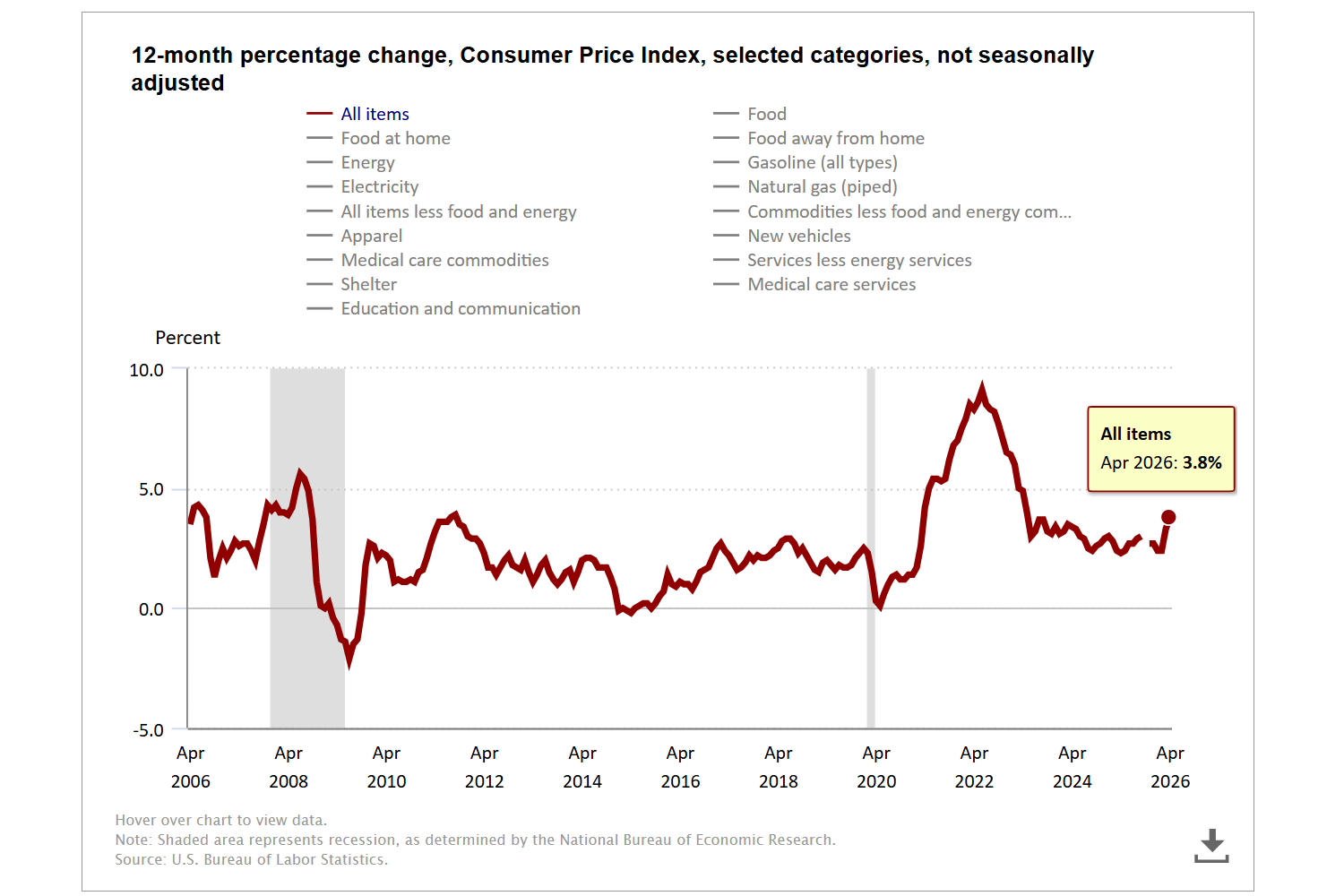

The April 2026 CPI number came in hot, confirming what most of us are feeling in our pocketbooks — rising prices.

The Consumer Price Index (CPI) for April crept up to 3.8%, the highest since May 2023.

Core Inflation, an adjusted number that excludes food and energy prices, rose to 2.8%.

This one isn’t as bad, but economists and politicians use this number to say “it’s not that bad, trust us”.

The Iran situation has caused fuel prices to rise, which will reverberate into other markets. Tariffs are still impacting supply chains, and how this shakes out, we don’t know. Things may get worse.

But frankly, when things get expensive, it doesn’t matter what’s expensive because it feels like you’re being nickel-and-dimed everywhere you turn.

Just this week, I paid $7 for a 20 oz. bottle of Orange Fanta.

I can’t believe 1) that I paid that much for a non-alcoholic drink, and 2) that it felt kind of normal to be gouged that way.

The credit card terminal asked if I wanted to tip 20%. I didn’t.

Our family likes amusement parks. So on a hot day riding roller coasters and sweating in the sun, I’ve decided just to accept the high costs for the one day I’m in the park (keeps me sane and the kids from complaining).

For the record, this wasn’t Disney. I’ve been to several Disney parks and their pricing almost seems reasonable compared to other parks we’ve been to.

Two summers ago, I paid $8.75 for one slice of pizza at a Disney property. The very next day, I spent $16 for one slice of pizza at a non-Disney park competitor.

The most shocking part: there was a line out the door, and I waited 30 minutes for a slice. The place selling $16 slices couldn’t find enough staff to cook more pizza at this absurd price.

I digress.

Inflation is detrimental to our wealth, but it’s hard to see in the near term, especially when the stock market is surging.

So you have to plan for it.

After seeing the April inflation numbers, I logged into my financial planning software (both Boldin and ProjectionLab) to review at my assumptions.

Sure enough, my plans are all set to a 2% long-term inflation rate.

That’s a rosy picture right now. As the national debt is rising out of control and politicians refuse to make meaningful changes to spending or revenues, it appears the government wants to “inflate their way” out of the national debt (topic for another day).

Instead of hoping for target inflation (2%) going forward, I’m adjusting all of my financial plans to assume 3%-4% going forward.

3% applied to one of the demo accounts I’ve used in YouTube videos didn’t significantly reduce the outcome.

But changing the assumption from 2% to 4% increased the odds of plan failure (run out of money) by quite a lot.

That’s the difference between leaving a substantial legacy and running out of money.

Running out of money is a scary phrase used in finance that is probably not the actual outcome. The more realistic outcome is forced spending reduction and discomfort, most likely when it hurts the most.

Retirees on a fixed income are feeling the pain today, but the pain is mostly offset by the rising stock market and home equity buffer.

But when the market turns, and inflation doesn’t, the pain will be widespread and real.

A market downturn would show an immediate impact to our DIY financial plans, while inflation is the slow killer.

Plan for it by adjusting your assumptions. I’m doing it permanently.

Favorite tools and investment services (Sponsored):

Boldin — Spreadsheets are insufficient. Build financial confidence. (review)

ProjectionLab — Build financial plans you love. (review)

Empower — Free net worth and portfolio tracking + retirement planning. User since 2015.

Sure Dividend — Research dividend stocks with free downloads (review):

Publisher: Source link