Health care costs are a top concern for the public, and there is widespread interest among lawmakers in making health care more affordable. Attention has increasingly focused on hospitals, which represent nearly one third of total health care spending and accounted for 40% of spending growth from 2022 to 2024. Hospital spending reflects both the prices paid for services and the volume and intensity of care delivered, and trends in both factors have implications for affordability and spending growth. The prices paid by private insurers are higher than Medicare rates on average—e.g., nearly double traditional Medicare rates for hospital services when averaging across studies, according to a prior KFF review—and vary across regions and across hospitals and payers within regions. These high prices affect households through higher premiums and cost sharing obligations and reduced wages for those with employer-sponsored health coverage.

There has been some discussion at both the national and state level about policies that could rein in hospital prices. One set of policies aims to do so by promoting competition and reducing consolidation in provider markets. A substantial body of evidence shows that hospital market consolidation has contributed to higher prices, with unclear effects on the quality of services provided. Another set of policies would rein in prices more directly, such as by capping the prices that providers can charge. For example, Indiana recently enacted a law that will eventually cap private insurance prices for the state’s nonprofit hospitals, and Oregon has capped hospital prices at 200 percent of traditional Medicare rates for its state employee plan since 2019.

To inform policy discussions related to hospital prices and price regulation, this brief describes the growth of prices paid by private insurers for hospital care relative to increases in Medicare payment rates from April 2019 through April 2026, using data from the Bureau of Labor Statistics (BLS) Producer Price Index (PPI). The analysis begins in 2019 to fully capture changes in prices during the pandemic. See Methods for more detail.

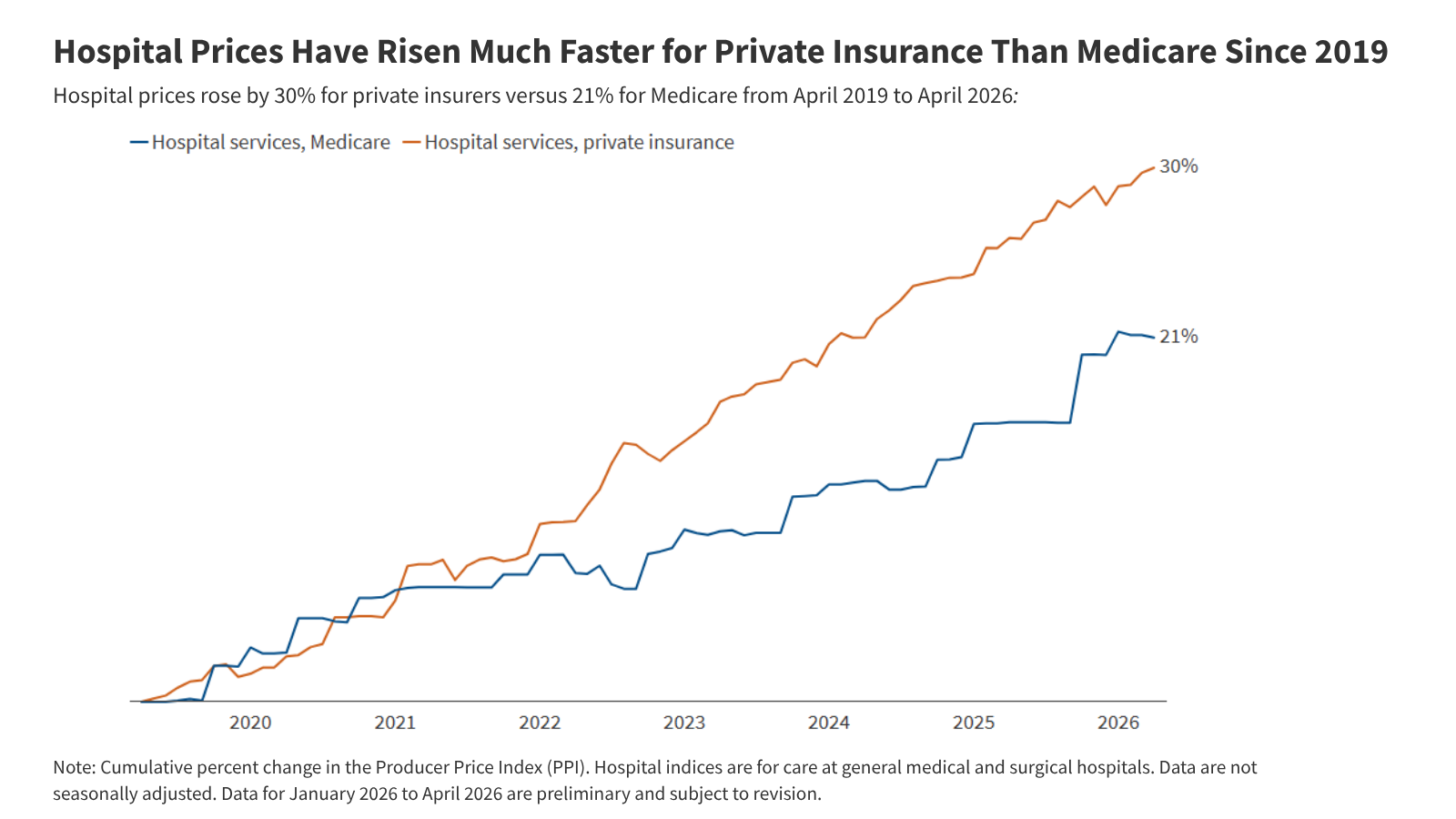

Hospital Prices Have Risen Much Faster for Private Insurance Than Medicare Since 2019

Private insurance prices for hospital care rose 30% from April 2019 to April 2026 compared to a 21% increase in Medicare rates (Figure 1). Put differently, private insurance prices grew 47% more quickly than Medicare rates over this 7-year period. Private insurance prices grew at a similar pace as Medicare rates from April 2019 to April 2020, but grew more quickly than Medicare rates each year from April 2020 to April 2025, before increasing less quickly than Medicare rates from April 2025 to April 2026. These patterns are broadly consistent with prior research that finds faster price growth for private insurance than Medicare over time, with some variation across time periods. Private plans pay much higher rates than Medicare for hospital services according to prior research, and this analysis suggests that the gap has increased over time.

Private insurance prices for hospital care are the result of negotiations between hospitals and insurers. Increases in private prices over time can reflect changes in the cost of providing care and in the bargaining power of hospitals relative to insurers, among other factors. Hospital markets have become increasingly consolidated, with one or two health systems controlling at least 75% of the market for inpatient hospital care in the large majority of metropolitan areas (83%) in 2024, according to KFF analysis, contributing to higher prices. Large increases in labor and supply expenses during the pandemic have likely pushed providers to negotiate for higher prices (economy-wide inflation jumped in March and April 2021 before reaching a peak in June 2022). However, contracts between hospitals and insurers are only periodically renegotiated, and often last for multiple years, meaning there may be a lag before any effects of higher input costs are fully reflected in higher prices.

In contrast, traditional Medicare hospital prices are updated annually by the Centers for Medicare and Medicaid Services (CMS), primarily through the Inpatient and Outpatient Prospective Payment Systems (IPPS and OPPS). These changes are based on factors and methods described in law and regulation. Medicare IPPS and OPPS updates are based partially on estimates of increases in hospital services input costs, which are affected by overall inflation. There is some evidence that rates paid by Medicare Advantage plans for hospital services (incorporated with other private Medicare plans in the Medicare but not private insurance PPI) are generally close to rates paid by traditional Medicare. Increases in prices paid by Medicare Advantage insurers have likely been aligned with changes in traditional Medicare rates over time.

One factor that slowed Medicare growth is that the program underestimated inflation in recent periods when prospectively setting rates (e.g., inflation in 2022 was much higher than expected when hospital rates were set for that year), according to the hospital industry and others. Nonetheless, CMS has noted that its forecasts have tended to be close to actual inflation on average when looking over longer periods for the IPPS hospital market basket (see Methods for more detail).

Various other factors may have restrained Medicare price growth during the study period, such as the productivity adjustments enacted under the Affordable Care Act, which reduce the growth in traditional Medicare rates over time under the assumption that hospitals are becoming more efficient at delivering care. As another example, sequestration, which is an automatic reduction in Medicare payments required under budget rules, was temporarily suspended during the pandemic beginning in May 2020 but gradually reintroduced in April and July 2022, likely contributing to the increase and decrease in the Medicare PPI during those periods.

Methods

This brief used the Producer Price Index (PPI) to evaluate hospital prices and overall inflation over the seven year period from April 2019 to April 2026 (the most recent month available). The PPI measures prices from the perspective of producers of a good or service, such as hospitals. The PPI was used over other comparable measures like the Consumer Price Index (CPI) because it breaks out hospital price growth by payers, such as Medicare and private insurance. The PPI for private insurance excludes private Medicaid and Medicare plans. The PPI for Medicare includes both traditional Medicare and private Medicare plans, including Medicare Advantage, which accounted for 54% of the eligible Medicare population in 2025.

Hospital price growth overall (i.e., across all payers) as measured by the PPI grew much less quickly than hospital price growth as measured by the CPI during this period. Differences between the PPI and CPI reflect both conceptual and methodological differences. For example, the CPI—which measures prices from the perspective of consumers—excludes Medicare Part A, Medicaid, and certain other payers from its price measurements.

This analysis examines hospital PPI data classified by industry, in this case, the hospital industry. The PPI also produces series classified by a specific commodity, such as a product or service. This brief uses industry classifications because they provide an overall measure of hospital prices by payer, while the commodity classifications are separated into inpatient and outpatient price measures and only distinguish private insurers from other non-Medicare, non-Medicaid payers for the former.

Most of the increases in the Medicare hospital PPI occur in October and January over time. That likely reflects, at least in large part, the timing of when traditional Medicare updates inpatient and outpatient reimbursement for hospitals, respectively.

CMS noted in its FY2026 IPPS rule that its forecasts for the IPPS hospital market basket have tended to be close to actual inflation on average when looking over longer periods. This basket is used for both IPPS operating and OPPS payment updates (though it is unclear if CMS’s comment above was also including OPPS payments, which are updated on a different schedule). During the 2026 rulemaking process, CMS received comments, including from the hospital industry, recommending an increase in IPPS operating and OPPS payment rates to account for prior errors in forecasting, though CMS did not do so, citing various reasons. CMS does make certain adjustments for forecasting errors for IPPS capital payments (as it has proposed to do in FY2027), which account for a relatively small share of hospital payments.

Publisher: Source link