Virtually all enrollees in Medicare Advantage (99%) are required to obtain prior authorization for some services – most commonly, higher cost services, such as inpatient hospital stays, skilled nursing facility stays, and chemotherapy. This contrasts with traditional Medicare, where only a limited set of services require prior authorization. Prior authorization requirements are intended to ensure that health care services are medically necessary by requiring approval before a service or other benefit will be covered. Medicare Advantage insurers typically use prior authorization, along with other tools, such as provider networks, to manage utilization and lower costs. This may contribute to their ability to offer extra benefits and reduced cost sharing, typically for no additional premium, while maintaining strong financial performance.

Some lawmakers and others have raised concerns that prior authorization requirements and processes, including the use of artificial intelligence to review requests, impose barriers and delays to receiving necessary care. In response to some of these concerns, the Centers for Medicare and Medicaid Services (CMS) recently finalized three rules. Among other changes, the three rules clarify the criteria that may be used by Medicare Advantage plans to establish prior authorization policies, streamline the prior authorization process for Medicare Advantage and certain other insurers, and require Medicare Advantage plans to evaluate the effect of prior authorization policies on people with certain social risk factors. Additionally, lawmakers in Congress have introduced several bills to reform various aspects of prior authorization (see Box 1 at the end).

To inform ongoing discussions about the use of prior authorization, this analysis uses data submitted by Medicare Advantage insurers to CMS to examine the number of prior authorization requests, denials, and appeals for 2019 through 2022, as well as differences across Medicare Advantage insurers in 2022.

Key Takeaways:

- More than 46 million prior authorization requests were submitted to Medicare Advantage insurers on behalf of Medicare Advantage enrollees in 2022, up from 37 million in 2019.

- In 2022, there were 1.7 prior authorization requests per Medicare Advantage enrollee, similar to the amount in 2019. The rise in the total number of prior authorization requests corresponded to increasing enrollment in Medicare Advantage and so translated into a similar number of requests per enrollee.

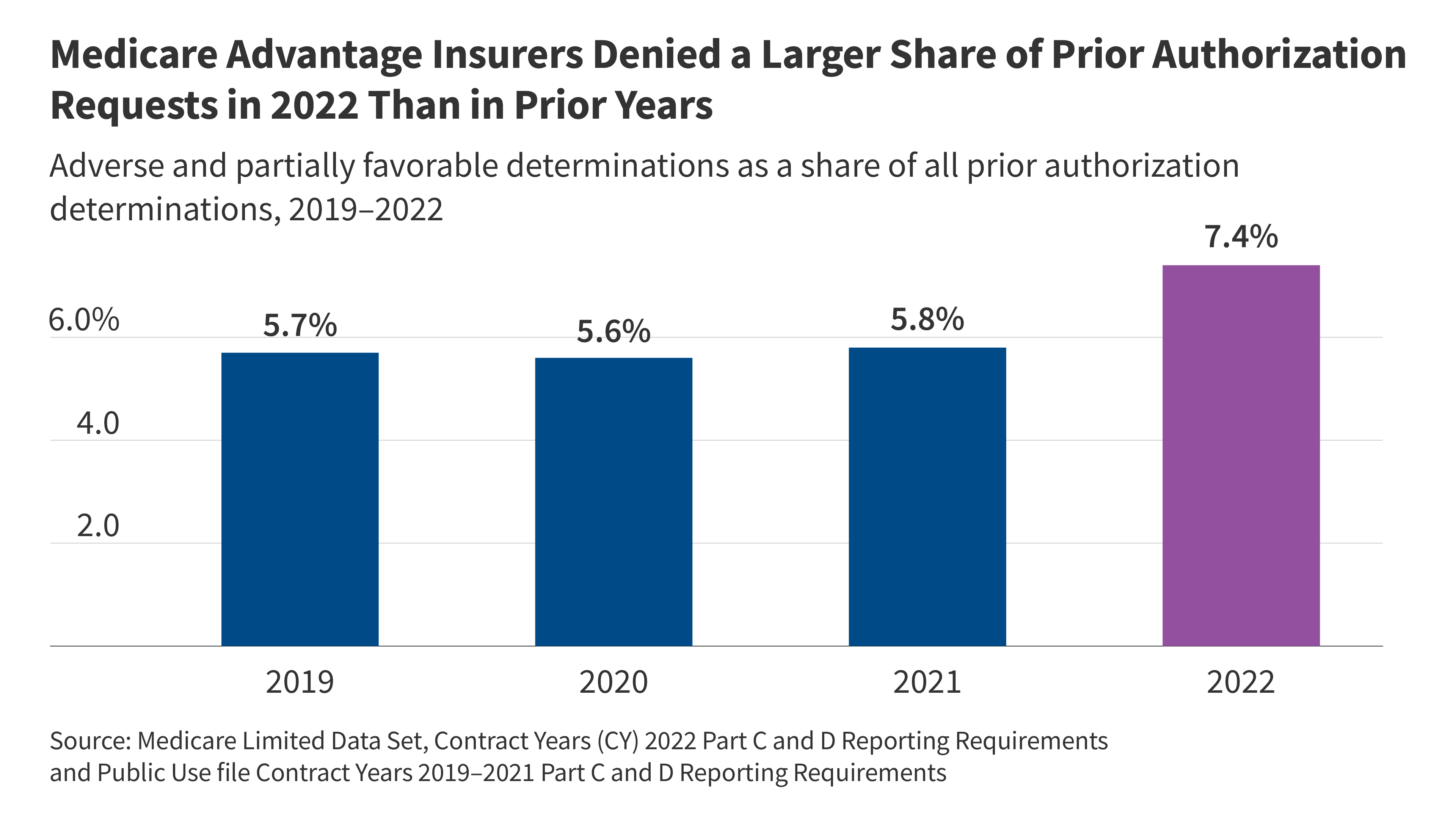

- In 2022, insurers fully or partially denied 3.4 million (7.4%) prior authorization requests. Though insurers approved most prior authorization requests, the share of requests that were denied jumped between 2021 and 2022. The share of all prior authorization requests that were denied increased from 5.7% in 2019, 5.6% in 2020 and 5.8% in 2021 to 7.4% in 2022.

- Just one in ten (9.9%) prior authorization requests that were denied were appealed in 2022. That represents an increase since 2019, when 7.5% of denied prior authorization requests were appealed. The low rate of appeals may be attributed to enrollees not knowing that they can appeal a denial or finding the appeal process intimidating. A prior KFF survey found that many people who experience denials, including those with Medicare, are confused by their coverage and don’t know how to file an appeal with their plan.

- The vast majority of appeals (83.2%) resulted in overturning the initial prior authorization denial. Though a small share of prior authorization denials were appealed, more than 80% of appeals resulted in partially or fully overturning the initial decision in 2022, and in each year between 2019 and 2021. These requests represent medical care that was ordered by a health care provider and ultimately deemed necessary but was potentially delayed because of the additional step of appealing the initial prior authorization decision. Such delays may have negative effects on a person’s health.

- Medicare Advantage insurers vary in their use of prior authorization. In 2022, the volume of prior authorization determinations varied across Medicare Advantage insurers, as did the share of requests that were denied, the share of denials that were appealed, and the share of decisions that were overturned upon appeal, meaning people may have different experiences depending on the Medicare Advantage plan in which they enroll.

Use of Prior Authorization in Medicare Advantage

As part of its oversight of Medicare Advantage plans, CMS requires Medicare Advantage insurers to submit data for each Medicare Advantage contract (which usually includes multiple plans) that includes the number of prior authorization determinations made during a year, and whether the request was approved. Insurers are additionally required to indicate the number of initial decisions that were appealed (reconsiderations) and the outcome of that process. These data are useful for assessing overall and insurer level trends, but do not contain the information necessary to understand how the use of prior authorization varies by type of service or type of plan.

In 2022, more than 46 million prior authorization requests were submitted to Medicare Advantage insurers.

After dropping in 2020 amid the initial phase of the COVID-19 pandemic, prior authorization requests increased steadily (Figure 1). The decline in 2020 was likely due to both a decline in utilization, as well as some insurers’ decision to temporarily pause prior authorization requirements during the public health emergency.

The recent increase in the total number of prior authorization requests corresponds to an increase in Medicare Advantage enrollment. Between 2019 and 2022, the number of Medicare Advantage enrollees rose from 22 million people to 28 million people. In 2019, there were approximately 1.7 prior authorization requests per Medicare Advantage enrollee. That number dropped at the onset of the COVID-19 pandemic to 1.4 in 2020 and 1.5 in 2021, before returning to the pre-pandemic level of 1.7 requests per enrollee in 2022 (Figure 2).

Medicare Advantage insurers denied 3.4 million (7.4%) prior authorization requests in 2022.

Of the 46.2 million prior authorization determinations in 2022, more than 90% (42.7 million) were fully favorable, meaning the requested item or service was approved in full. The remaining 3.4 million (7.4%) were denied in full or in part. In comparison, between 2019 and 2021, less than 6% of prior authorization requests were denied (Figure 3). Across all years, adverse determinations, in which the request was denied in full, represented the majority of denials. In each year, a smaller share of determinations were partially favorable, meaning that only part of the request was approved. For example, the insurer may have approved 10 of 14 requested therapy sessions.

Just 9.9% of denied prior authorization requests were appealed in 2022.

The majority of the 3.4 million denied prior authorization requests were not appealed, similar to previous years. In 2019, just 7.5% of all denials were appealed. That share increased somewhat in 2020 to 10.2% and was relatively stable in 2021 (10.6%) and 2022 (9.9%) (Figure 4). These include appeals of claims that were both fully and partially denied.

The vast majority of denied prior authorization requests that were appealed were subsequently overturned.

From 2019 through 2022, more than eight in ten denied prior authorization requests that were appealed were overturned. That share was slightly higher in 2022 (83.2%) than in 2019 (81.6%), 2020 (81.4%) and 2021 (81.3%) (Figure 5). This raises questions about whether the initial request should have been approved, although it could also indicate that the initial request was missing the required documentation to justify the service. In either case, patients potentially faced delays in obtaining services that were ultimately approved because of the prior authorization process.

Variation in Use of Prior Authorization Across Medicare Advantage Insurers in 2022

While all Medicare Advantage insurers require prior authorization for at least some services, there is variation across insurers and plans in the specific services subject to these requirements. In addition, insurers have the option of waiving prior authorization requirements for certain providers, for example, as part of risk-based contracts or through “gold carding” programs that exempt providers with a history of complying with the insurer’s prior authorization policies.

Prior authorization requests were most common among Humana plans.

The number of prior authorization requests per enrollee ranged from a low of 0.5 requests per enrollee in Kaiser Permanente plans to a high of 2.9 requests per enrollee in Humana plans (Figure 6). Kaiser Permanente is atypical among insurers in that it generally operates its own hospitals and contracts with an affiliated medical group. Looking across insurers that are more similar, the low end of the range was 0.9 requests per enrollee in both Cigna and UnitedHealthcare plans. Differences across Medicare Advantage insurers in the number of prior authorization requests per enrollee likely reflect some combination of differences in the services subject to prior authorization requirements, the frequency with which contracted providers are exempted from those requirements, how onerous the prior authorization process is for a particular insurer relative to others, and differences in enrollees’ health conditions and the health care services they use.

CVS denied the highest share or prior authorization requests.

The denial rate ranged from 4.2% of prior authorization requests for Anthem plans to 13.0% of prior authorization requests for CVS plans (Figure 7). The overall denial rate includes requests that were both fully and partially denied (adverse and partially favorable determinations, respectively).

Most insurers that had more prior authorization requests per enrollee than average denied a smaller share of those requests than average and vice versa. The exceptions were Centene, which had both a relatively high number of prior authorization requests (2.2 per enrollee) and above average denial rates (9.5%), and Cigna, which had one of the lowest number of requests per enrollee (0.9) and denial rates (5.8%) that were also below average.

Across most insurers, a small share of denials were appealed.

Across most Medicare Advantage insurers, a small share of denied prior authorization requests were appealed. The exception was Cigna, in which 50.4% of all denials were appealed. Across other insurers, the shares ranged from 3.5% for Kaiser Permanente to 15.2% for BCBS Anthem (Figure 7). The substantial variation may reflect differences in both the prior authorization request and the appeals processes across insurers. For example, Cigna also had one of the lowest number of prior authorization requests per enrollee and denied a below average share of requests. Altogether, the number of appeals per enrollee among people enrolled in Cigna plans was more similar to those enrolled in plans sponsored by other insurers than the appeals rate might suggest. The differences could present challenges for providers who generally must interact with multiple private insurers. Alternatively, it could reflect differences in how the insurers interpreted the data reporting requirements. The high rate of appeal across Cigna plans is very much an outlier. Unfortunately, the data do not allow for a more in-depth examination because they lack additional detail.

Across all firms, at least two-thirds of appeals were successful.

Even though most denials were not appealed, when they were, most of the initial decisions were partially or fully overturned. The share of appeals that resulted in favorable decisions was lowest for Humana (68.4%). Two insurers overturned more than 9 in 10 of the initial decisions that were appealed, with CVS overturning 90.8% and Centene overturning 95.3% of denials upon appeal (Figure 9).

Box 1: Recent Administrative Actions and Proposed Legislation on Prior Authorization

The Administration recently finalized three rules related to prior authorization.

The first rule (effective date: June 5, 2023) clarifies the criteria that may be used by Medicare Advantage plans in establishing prior authorization policies and the duration for which a prior authorization is valid. Specifically, the rule states that prior authorization may only be used to confirm a diagnosis and/or ensure that the requested service is medically necessary and that private insurers must follow the same criteria used by traditional Medicare. That is, Medicare Advantage prior authorization requirements cannot result in coverage that is more restrictive than traditional Medicare. The rule also describes how private insurers may consider additional information when traditional Medicare does not have fully established coverage criteria. The rules apply to coverage beginning with plan year 2024.

The second rule (effective date: April 8, 2024) is intended to improve the use of electronic prior authorization processes, as well as the timeliness and transparency of decisions, and applies to Medicare Advantage and certain other insurers. Specifically, it shortens the standard time frame for insurers to respond to prior authorization requests from 14 to 7 calendar days starting in January 2026 and standardizes the electronic exchange of information by specifying the prior authorization information that must be included in application programming interfaces starting in January 2027. A bipartisan bill has also been introduced to codify pieces of this rule.

The third rule (effective date: June 3, 2024) will require Medicare Advantage plans to evaluate the effect of prior authorization policies on people with certain social risk factors starting with plan year 2025.

Additionally, lawmakers in Congress have introduced several bills aimed at improving the timeliness of the prior authorization process, increasing transparency, clarifying the criteria that may be used in prior authorization decisions, and exempting some providers from prior authorization requirements in the Medicare Advantage program. Other lawmakers have proposed banning the use of prior authorization altogether.

This work was supported in part by Arnold Ventures. KFF maintains full editorial control over all of its policy analysis, polling, and journalism activities.

| Methods |

| This analysis uses organization determinations and reconsiderations – Part C data from the Centers for Medicare and Medicaid Services (CMS) Part C and D reporting requirements public use file for contract years 2019 – 2021 and the limited data set for contract year 2022. Medicare Advantage insurers submit the required data at the contract level to CMS and CMS performs a data validation check.

This analysis reflects data on service determinations and do not include claims determinations (for payment for services already provided). We also do not include withdrawn or dismissed determination requests in this analysis. The enrollment data are from the CMS Medicare Advantage enrollment file for March of each year at the contract-plan-county level. We then sum up to the contract level to merge with the determination and reconsideration data. Contract-plan-county combinations are not included if there are fewer than 11 enrollees. |

Publisher: Source link